Should I Use a Mortgage Broker?

(especially as a high or complex earner)

Lenders' publicly available affordability calculators will tell you one number. Their actual underwriting policy, if you had access to them, might tell you something very different. And that’s the crux of the decision.

The common misconception about mortgage brokers is that you should use one because they have access to mortgages and rates not available direct to retail customers. While there are some broker-exclusive deals, in practice they’re a tiny percentage of the market and broadly speaking don’t offer anything you couldn’t find elsewhere.

This gap between public and private lending criteria is the real reason to consider using a mortgage broker. Not because they have access to exclusive rates (they mostly don’t), but because they understand how different lenders actually assess complex applicants.

The real value: matching you to the right lender

If you’ve got a simple situation: A good credit record, a bog-standard fixed salary, decent LTV, then you can probably use an online comparison service to find who’ll give you the best rates.

But once you add any complexity at all - be it bonuses, commission, RSUs, maternity leave, self-employment, visa status, or wanting a lender to consider your investment portfolio, suddenly the landscape becomes far more complex to navigate especially if you have multiple factors that come into play.

Once you get beyond the basics, how lenders underwrite you varies massively. And crucially, much of that underwriting policy isn’t publicly available to retail customers. And this “secret” (or at least non-public) policy can make a huge difference to both the amount lenders are willing to lend and the rates you can get.

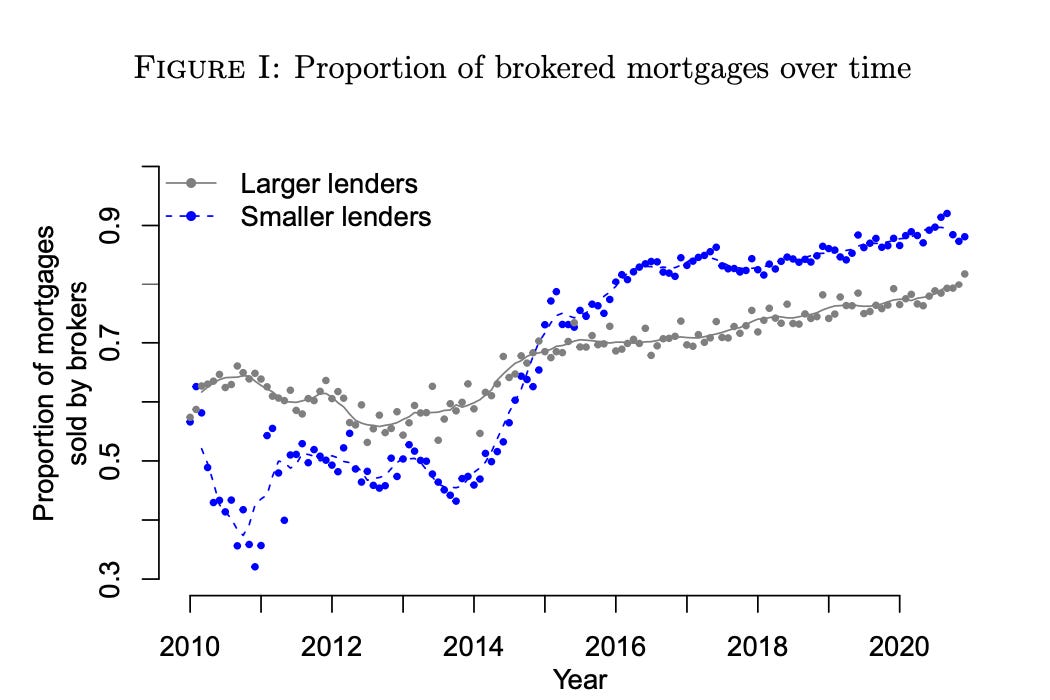

Historically almost all mortgages were provided by a handful of large banks with large networks of bank branches to sell them, the rise of mortgage brokers has broken this stronghold with a quarter of mortgages being offered by smaller lenders. The best lender for you might well be a regional bank you’ve never heard of.

A good broker’s primary value is understanding the complexities of underwriting policies and matching you with the right lender for your specific situation.

What else does a broker do?

They manage the paperwork. The biggest thing that slows mortgage applications down is back-and-forth over missing documents. A good broker will guide you upfront on exactly what you need and do a first pass to identify potential stumbling blocks before the lender even sees your application.

They have relationships at lenders. If something about your application isn’t obviously acceptable, brokers have contacts they can call to get the inside view. For larger mortgages (thresholds vary by lender, but often £500k or £1m), they may be able to speak with an underwriter directly. If you’ve got a complex situation where a conversation can help, this can be the difference between getting a mortgage and not.

Should I trust a mortgage broker?

Broadly speaking, whole-of-market mortgage brokers (the only kind worth considering) are aligned with your interests. They make money by securing you a mortgage, at which point they receive a commission from the lender (and depending on the broker, may also charge you a fee).

Because they’re compensated on completion, they’re genuinely motivated to get your mortgage across the line. Around 75% of broker applications complete, with most drop-outs being buyers who decide not to proceed with a house purchase rather than application failures. Brokers generally want to avoid submitting an application unless they’ve got good confidence it’ll be approved, otherwise they end up doing the work and not making any money from it.

That said, there are a few incentive misalignments worth being aware of:

Loan size. Broker commissions are typically a percentage (often around ~0.35%) of the loan amount, so there’s a structural incentive toward larger mortgages. Brokers won’t aggressively push you to borrow more, but they’re unlikely to nudge you toward borrowing less.

Fixed term length. Brokers get paid per mortgage, including remortgages. They’ll typically earn the same commission whether you take a two-year or five-year fix, but a two-year deal means potentially another remortgage (and another commission) in two years’ time. This doesn’t mean a two-year fix is wrong for you, but it’s worth knowing where the incentive sits.

Add-on products. Many brokers also sell life insurance and income protection. Some of these can be sensible, but make your own judgement rather than relying solely on your broker’s recommendation, this is where their incentives are least aligned with yours.

What’s the advantage of going direct?

Simplicity. Removing an intermediary may make things faster and reduce errors. A bad broker who slows down the process and makes mistakes is definitely worse than going direct.

But there’s a catch: the market is almost entirely shifting to being broker-led. This isn’t to say you should use a broker because everyone else does, but it has had a direct impact on banks’ ability to serve you well when you go direct.

There was a time when you could walk into a high-street bank and have a mortgage appointment with a manager who handled the mortgages for most people locally and had seen everything in their time. Nowadays you’re more likely to speak with someone with far more limited mortgage experience.

My own experience with the “high earner” team at a major high-street bank was dispiriting: staff made basic mistakes explaining their own bank’s lending policies, leaving me with little confidence in their ability. I ended up going elsewhere.

If you do go direct, you’re likely better off skipping the branch, self-educating and using the lender's online application instead. Most branch staff won’t have the expertise to advise on anything beyond the basics.

The bottom line

For most readers with complex situations or larger loans, a good broker will likely save you time and potentially money. The question isn’t whether to use one, but how to find the right one for you, and that’s what we’ll be covering in our next article.